Fed Vice Chair Questioned on Banks’ Stablecoin Engagement as Framework Nears

SAFE/USDT

$19,384,548.40

$0.1706 / $0.1419

Change: $0.0287 (20.23%)

+0.0050%

Longs pay

Contents

The GENIUS Act stablecoin regulation empowers the Federal Reserve to develop frameworks for digital assets, allowing banks to engage fully while ensuring stability. Signed into law in July 2025, it addresses stablecoin oversight amid congressional scrutiny over definitions and volatility risks.

-

GENIUS Act Overview: Authorizes Federal Reserve to regulate payment stablecoins, promoting safe banking integration.

-

Federal Reserve Vice Chair Michelle Bowman supports banks exploring digital assets to understand the technology.

-

FDIC plans to propose stablecoin supervision rules later this month, including issuer requirements, per acting chair Travis Hill.

Discover how the GENIUS Act stablecoin regulation shapes Federal Reserve policies on digital assets. Learn about oversight hearings and upcoming frameworks for safer crypto banking integration. Stay informed on key developments.

What is the GENIUS Act and its role in stablecoin regulation?

The GENIUS Act stablecoin regulation is a landmark bill signed into law by US President Donald Trump in July 2025, directing federal agencies like the Federal Reserve and FDIC to establish rules for payment stablecoins. It aims to provide a clear framework for banks to handle these assets securely, distinguishing them from volatile cryptocurrencies. This legislation responds to the growing need for regulatory clarity in the digital asset space.

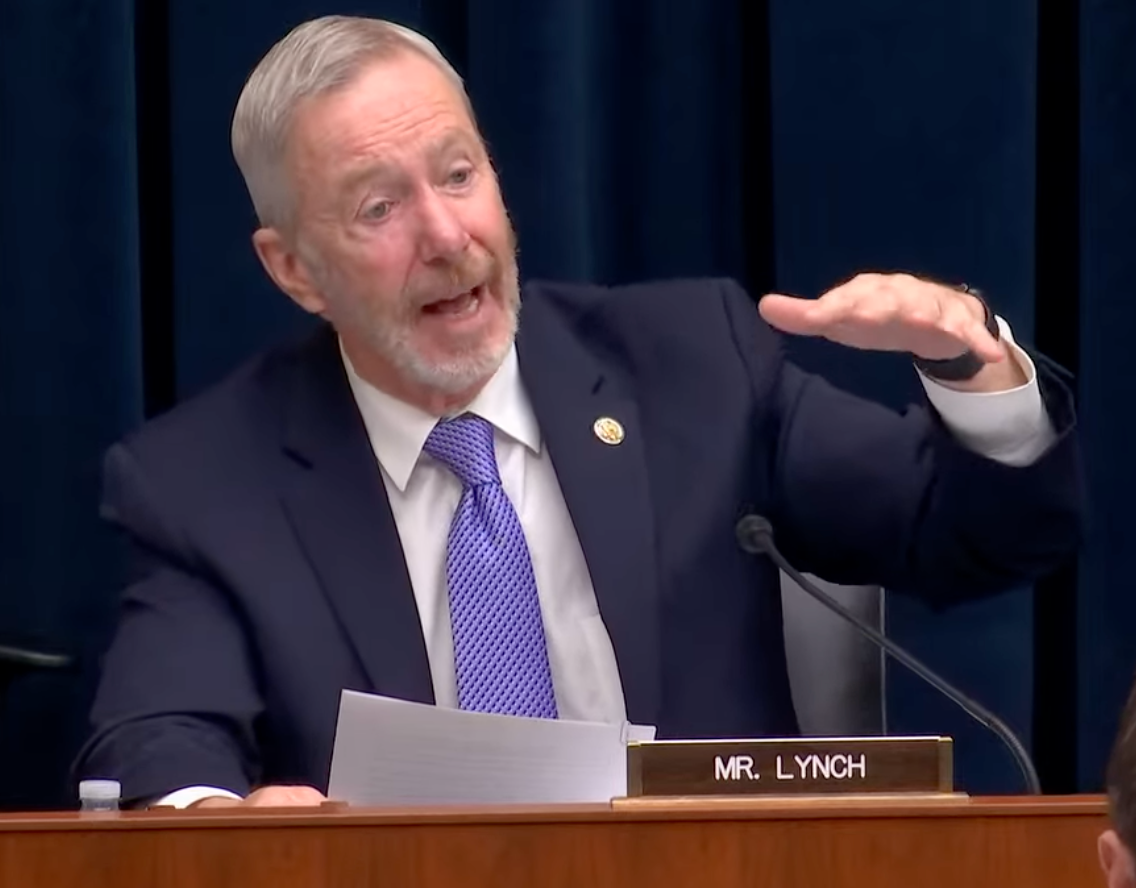

In a recent oversight hearing, US Representative Stephen Lynch questioned Federal Reserve Vice Chair for Supervision Michelle Bowman about her earlier comments encouraging banks to “engage fully” with digital assets. Bowman had made these remarks at the Santander International Banking Conference in November, emphasizing the importance of understanding technologies like stablecoins. The discussion highlighted the Federal Reserve’s evolving stance, authorized by the GENIUS Act to promulgate necessary regulations.

Representative Stephen Lynch at Tuesday’s oversight hearing. Source: House Financial Services Committee

Stablecoins, typically pegged to fiat currencies like the US dollar, maintain relative price stability, rarely deviating more than 1% from their peg under normal conditions. Historical events, such as the 2022 collapse of Terra’s algorithmic stablecoin, underscore the risks of depegging, but most collateralized stablecoins have proven resilient. Bowman’s comments reflect a broader push within the Federal Reserve to educate staff on these assets, as she noted in August that employees should hold small amounts of crypto or digital assets for better comprehension.

How does the Federal Reserve distinguish digital assets from stablecoins?

The Federal Reserve views digital assets broadly as any tokenized representations of value, including cryptocurrencies, tokens, and stablecoins, but emphasizes distinctions based on stability and utility. Stablecoins, as defined under the GENIUS Act, are specifically designed for payments and must maintain a stable value, often backed by reserves. Bowman clarified during the hearing that while digital assets encompass volatile cryptocurrencies, stablecoins require targeted regulation to mitigate systemic risks.

Expert analysis from financial regulators highlights that this separation is crucial for banking integration. For instance, the Act mandates reserves and redemption mechanisms for stablecoin issuers, drawing from guidelines issued by the Office of the Comptroller of the Currency. Statistics show the stablecoin market exceeding $150 billion in circulation as of late 2025, with over 90% pegged to the dollar, per data from blockchain analytics firms. Bowman reiterated the Fed’s congressional mandate: “The GENIUS Act requires us to promulgate regulations to allow these types of activities,” ensuring supervised engagement without endorsing speculation.

During the Tuesday hearing before the House Financial Services Committee, Lynch expressed confusion over terminology, probing Bowman on whether her support extended to all digital assets or just stablecoins. Bowman responded by outlining the Fed’s supervised framework, which prioritizes risk assessment. This exchange underscores ongoing congressional oversight, with lawmakers like Lynch pushing for precise definitions to prevent regulatory gaps.

Atkins, a securities expert, has stated that the SEC possesses sufficient authority to advance crypto rules in 2026, complementing the GENIUS Act’s focus. Similarly, the hearing featured testimony from FDIC Acting Chair Travis Hill, who announced plans for a stablecoin framework proposal later this month. This framework will outline supervision requirements for issuers, aligning with the Act’s goals of consumer protection and financial stability.

The FDIC’s role is pivotal, as it insures deposits and monitors banking risks associated with digital assets. Hill emphasized that the proposal would address custody, reserve management, and anti-money laundering compliance for stablecoin operations. With the GENIUS Act now law, agencies are moving swiftly; the FDIC’s timeline suggests implementation could begin in early 2026, providing banks with actionable guidelines.

Crypto projects often navigate conflicts between privacy features and anti-money laundering laws, a challenge that the GENIUS Act indirectly addresses through its supervisory mandates. By requiring transparency in stablecoin operations, the legislation balances innovation with accountability, as noted in regulatory discussions.

Frequently Asked Questions

What does the GENIUS Act stablecoin regulation mean for banks?

The GENIUS Act enables banks to engage with stablecoins under federal oversight, requiring reserves and stability measures to prevent risks like depegging. It authorizes the Federal Reserve and FDIC to create rules, allowing safe integration into traditional banking while protecting depositors from volatility.

How will the FDIC’s stablecoin framework impact the crypto market?

The FDIC’s upcoming framework will introduce supervision for stablecoin issuers, focusing on reserves, audits, and compliance to ensure market stability. This natural progression under the GENIUS Act will likely boost confidence, encouraging more institutional adoption of dollar-pegged stablecoins for payments and remittances.

Key Takeaways

- Regulatory Clarity from GENIUS Act: Provides a structured approach for stablecoin oversight, distinguishing them from volatile digital assets and empowering federal agencies.

- Fed’s Encouragement for Engagement: Vice Chair Bowman advocates for banks and staff to explore digital assets responsibly, backed by the Act’s mandates.

- Upcoming FDIC Proposal: Expected later this month, it will detail issuer requirements, fostering safer crypto-banking integration.

Conclusion

The GENIUS Act stablecoin regulation marks a significant step in aligning Federal Reserve digital assets policies with the realities of modern finance, as evidenced by the recent oversight hearing involving Representative Lynch and Vice Chair Bowman. By clarifying distinctions between stablecoins and broader digital assets, it paves the way for supervised innovation. As the FDIC advances its framework, stakeholders can anticipate enhanced stability and adoption; financial institutions are encouraged to prepare for these developments to capitalize on emerging opportunities in the crypto ecosystem.

Add COINOTAG as a Preferred Source

Add COINOTAG to your preferred sources in Google News and Search to see our coverage first.

Add on Google