UK Mandates Crypto Reporting for Domestic Users from 2026, Boosting Global Bitcoin Tax Oversight

BTC/USDT

$22,779,004,702.62

$74,664.97 / $72,582.82

Change: $2,082.15 (2.87%)

+0.0056%

Longs pay

Contents

The UK will mandate crypto platforms to report all transactions by domestic users starting in 2026 under the expanded Cryptoasset Reporting Framework (CARF), enabling HMRC to access comprehensive data on both domestic and cross-border activities to enhance tax compliance.

-

UK crypto platforms must report all user transactions from 2026, closing gaps in domestic oversight.

-

This expansion aligns with global CARF standards, facilitating automatic data exchange between tax authorities.

-

Supporting data shows 80% of OECD countries adopting similar measures by 2027, per OECD reports.

Discover how the UK’s 2026 crypto tax reporting rules will impact investors and platforms. Stay compliant and informed on global digital asset regulations with our guide—read on for essential insights.

What is the UK’s Crypto Reporting Framework Starting in 2026?

The UK crypto tax reporting 2026 initiative requires all domestic cryptocurrency platforms to disclose transaction details for UK-resident users, marking a significant expansion of the Cryptoasset Reporting Framework (CARF). Developed by the Organisation for Economic Co-operation and Development (OECD), CARF standardizes the automatic exchange of cryptoasset information across borders to combat tax evasion. This move ensures His Majesty’s Revenue and Customs (HMRC) gains full visibility into both local and international crypto activities, effective from 2026, ahead of the first global data exchanges in 2027.

How Does CARF Expand to Cover Domestic UK Crypto Transactions?

CARF traditionally emphasizes cross-border crypto transactions, requiring service providers to conduct due diligence, verify user identities, and submit annual reports on activities like transfers and exchanges. Under the new UK rules, this scope widens to include purely domestic dealings, preventing cryptocurrencies from evading the Common Reporting Standard (CRS) applied to traditional finances. HMRC’s policy paper highlights that this unified approach will simplify compliance for platforms while providing tax authorities with a holistic dataset to detect evasion. Experts from the OECD note that such frameworks have already recovered billions in unpaid taxes globally, with one analyst stating, “This closes the loop on digital assets, treating them like any other financial instrument.” Short sentences aid clarity: Platforms must now track all user wallets, report values in fiat equivalents, and face penalties for non-compliance up to 10% of unreported amounts.

The United Kingdom’s decision to implement these changes stems from a growing recognition of cryptocurrencies’ role in the economy. As digital assets gain mainstream adoption, governments seek to ensure fair taxation without stifling innovation. For UK users, this means enhanced transparency but also potential benefits like deferred capital gains under proposed DeFi rules. The “no gain, no loss” provision, announced alongside the reporting mandate, allows DeFi participants to postpone tax liabilities until token sales, a measure praised by industry leaders for reducing administrative burdens. According to HMRC estimates, crypto holdings in the UK exceeded £10 billion in 2024, underscoring the need for robust oversight.

Source: Cris Carrascoca

Governments Step Up Crypto Tax Oversight Worldwide

Globally, regulatory bodies are aligning on crypto taxation to match the sector’s rapid growth. The UK’s 2026 rollout is part of a broader trend where nations update policies to capture digital asset income effectively.

In South Korea, the National Tax Service has intensified enforcement, announcing in October plans to seize cryptocurrencies from cold wallets and perform home searches for evading taxpayers. This aggressive stance reflects concerns over undeclared gains, with officials reporting a 25% rise in crypto-related audits in the past year.

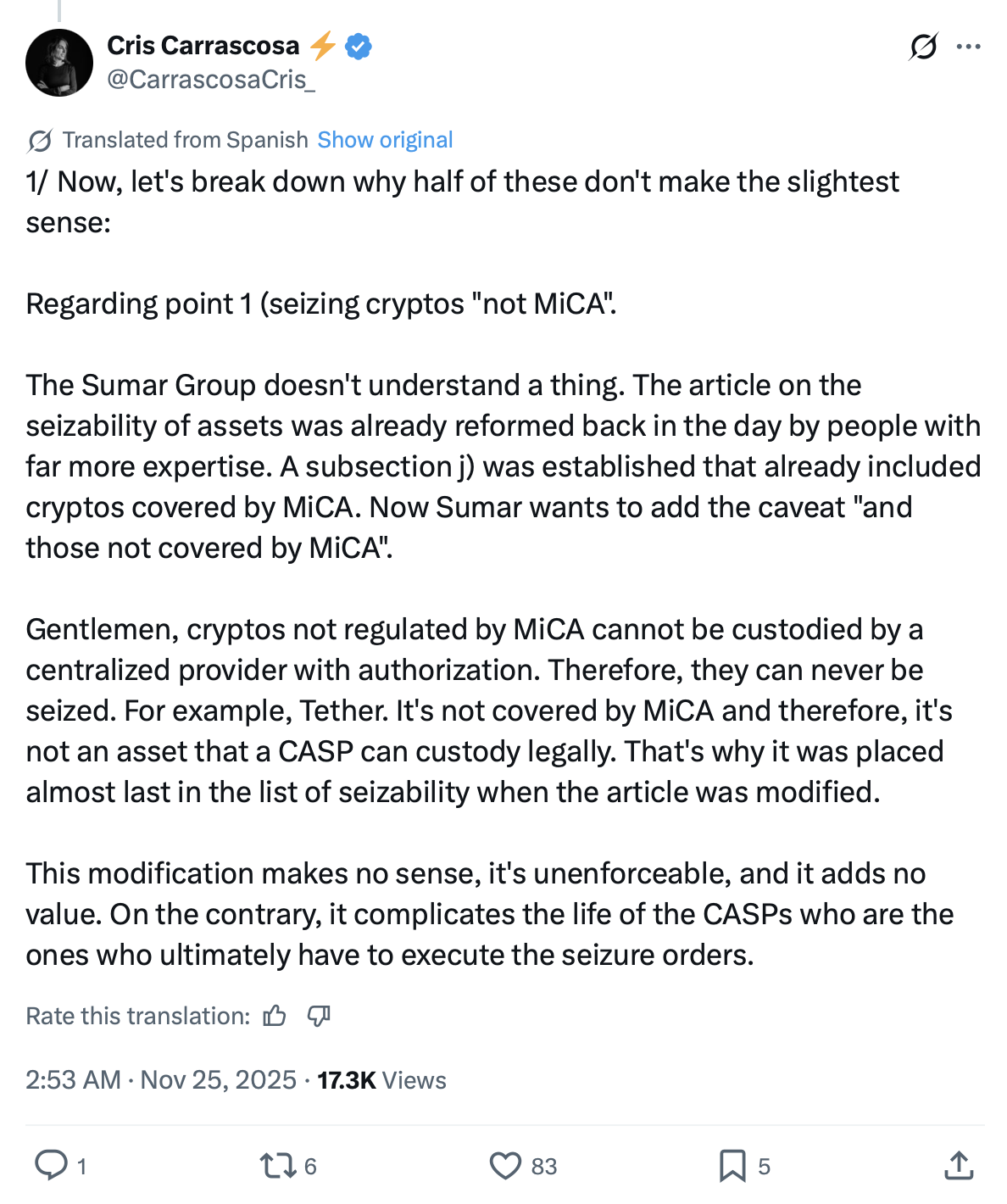

Spain’s recent proposals from the Sumar parliamentary group aim to elevate crypto gains taxes to a maximum 47%, integrating them into general income brackets while setting a 30% flat rate for corporations. Local reports indicate this could generate an additional €1.5 billion in revenue annually, addressing budget shortfalls amid economic pressures.

Switzerland, known for its crypto-friendly stance, has deferred automatic information exchanges under CARF until 2027, allowing time to select partner countries. While the rules integrate into Swiss law on January 1, transitional provisions will support local firms, ensuring a smooth shift without immediate disruptions.

Across the Atlantic, the United States is exploring innovative approaches. Representative Warren Davidson’s Bitcoin for America Act, introduced in November, permits federal tax payments in Bitcoin, directing funds to a national reserve. This bill treats such transactions as tax-neutral, exempting them from capital gains and potentially encouraging wider BTC adoption.

These developments illustrate a coordinated international effort. The OECD’s CARF, now endorsed by over 50 jurisdictions, standardizes reporting to foster trust in digital markets. UK officials emphasize that the changes promote fairness, preventing high-net-worth individuals from using crypto to obscure wealth. Industry responses vary: While some executives, like Kraken’s co-CEO, caution that overly stringent rules could hinder user protection, others welcome the clarity it brings.

Related: Kraken co-CEO warns UK rules meant to protect users punish them.

Magazine: Koreans ‘pump’ alts after Upbit hack, China BTC mining surge: Asia Express.

From a compliance perspective, crypto firms must now invest in advanced reporting systems. Tools for KYC (Know Your Customer) and transaction monitoring will become essential, potentially increasing operational costs by 15-20%, per industry analyses from firms like Deloitte. However, this could level the playing field, as smaller platforms gain from standardized processes.

Frequently Asked Questions

What Changes for UK Crypto Users Under the 2026 Tax Reporting Rules?

Starting in 2026, UK residents’ crypto transactions on domestic platforms will be automatically reported to HMRC, including details on buys, sells, and transfers. This ensures accurate capital gains assessments, with users required to maintain records for up to six years; non-compliance risks fines up to £300 per unreported transaction, based on HMRC guidelines.

Will the UK’s CARF Expansion Affect DeFi Activities?

Yes, the framework now includes DeFi under the “no gain, no loss” rule, deferring taxes until tokens are sold for fiat or goods. This natural approach simplifies DeFi for everyday users, allowing seamless participation while HMRC tracks underlying assets for eventual taxation.

Key Takeaways

- Enhanced Domestic Reporting: UK platforms must disclose all local crypto activities from 2026, bolstering HMRC’s oversight.

- Global Alignment: CARF adoption by the UK mirrors actions in South Korea, Spain, and others, promoting consistent international standards.

- DeFi Tax Relief: New rules defer capital gains for DeFi users, encouraging innovation while ensuring eventual compliance.

Conclusion

The UK’s crypto tax reporting 2026 expansion under CARF represents a pivotal step in integrating digital assets into traditional tax systems, complemented by global efforts in nations like South Korea and Spain. By providing HMRC with comprehensive data, these measures aim to foster a transparent ecosystem that protects public revenues without impeding growth. As regulations evolve, crypto investors should prepare for heightened compliance—consulting tax professionals now can safeguard against future liabilities and unlock opportunities in this dynamic landscape.

Add COINOTAG as a Preferred Source

Add COINOTAG to your preferred sources in Google News and Search to see our coverage first.

Add on GoogleRelated Tags

Comments

Other Articles

Saylor’s Strategy Adds $963M in Bitcoin as BitMine Boosts ETH Holdings

December 9, 2025 at 01:53 PM UTC

China Targets Tether-Led Stablecoins as Risks to Monetary Sovereignty Amid Crypto Crackdown

December 5, 2025 at 06:33 AM UTC

Kiyosaki Sells Bitcoin Portion for Real Assets, Eyes Future Accumulation

November 22, 2025 at 11:03 AM UTC